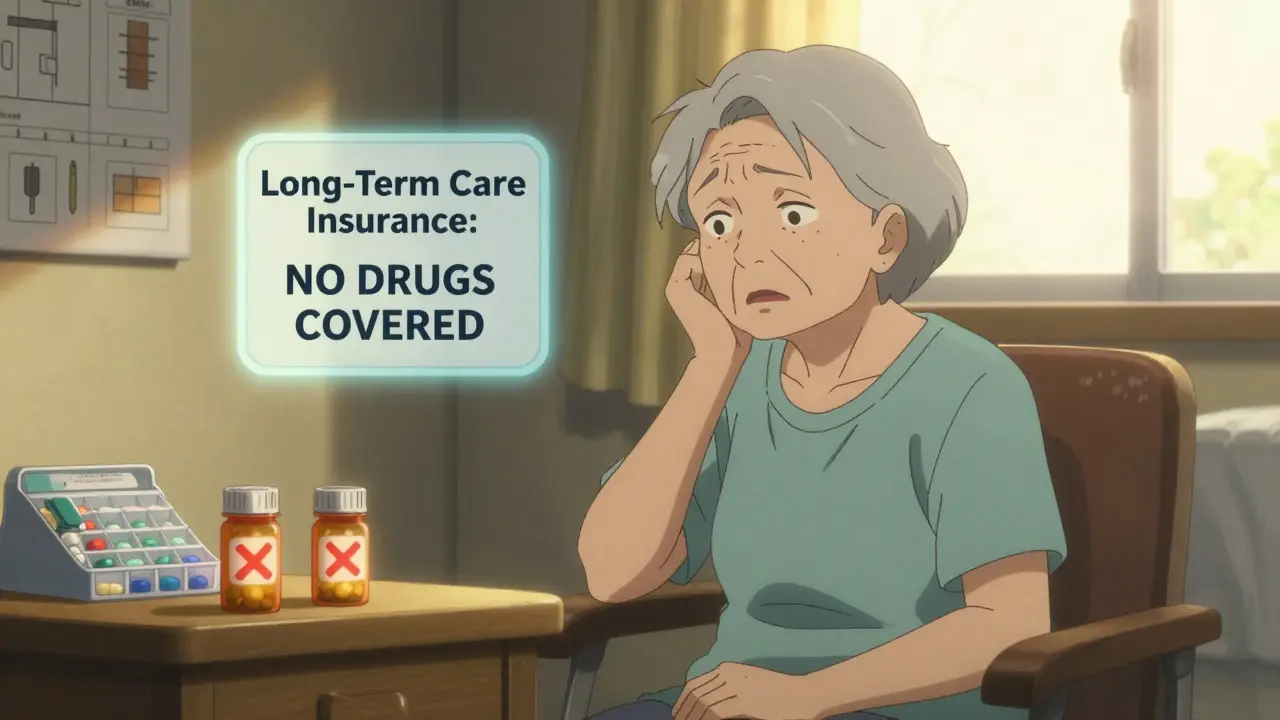

Many people assume that if they have long-term care insurance, it will pay for everything that comes with nursing home life-room, meals, physical therapy, and yes, even their daily pills. But here’s the hard truth: long-term care insurance does not cover prescription drugs, not even generic ones. That’s not a loophole. It’s by design.

What Long-Term Care Insurance Actually Covers

Long-term care insurance is meant to pay for help with everyday tasks when you can’t do them on your own. That means bathing, dressing, eating, moving from bed to chair, or using the toilet. It covers the cost of a nursing home room, assisted living services, or in-home care. But it draws a clear line at medical care. Medications? That’s not custodial care. That’s medical treatment. And medical treatment falls under health insurance, not long-term care insurance. If you’re in a nursing home and your policy says it covers "all care," read the fine print. Most policies explicitly exclude drugs, doctor visits, hospital stays, and diagnostic tests. Even if you’re in a facility paid for by your long-term care policy, your blood pressure pill, your diabetes medication, your antibiotic-those are not included. You’ll need something else to pay for them.Who Pays for Generic Drugs in Nursing Homes?

The real answer is Medicare Part D. Since it launched in 2006, Medicare Part D has become the primary payer for prescription drugs in nursing homes. According to data from a 2020 study, 82.4% of all drug costs for long-stay Medicare residents are covered by Part D plans. That’s more than eight out of every ten pills taken in a nursing home. Part D plans cover both brand-name and generic drugs-but they pay less for generics. That’s by design. Generic drugs are cheaper, so the plans encourage their use. Most Part D formularies list generics as Tier 1 drugs, meaning the lowest copay. A typical copay for a 30-day supply of a generic blood pressure pill might be $5 or less. The same brand-name drug could cost $40 or more. For residents who qualify for both Medicare and Medicaid (called "dual eligibles"), Part D still pays for drugs. Medicaid steps in only if the person isn’t enrolled in Part D-which is rare now. In fact, most nursing homes bill Medicare Part D directly for drugs, not Medicaid.What About Medicaid and Private Insurance?

Medicaid pays for drugs for residents who don’t qualify for Medicare. In those cases, Medicaid covers the cost of the drug at its acquisition price, plus a small dispensing fee. But this only applies to a small group. Most nursing home residents are on Medicare, not Medicaid. Private insurance? It’s a footnote. Only 8.5% of nursing home drug costs are covered by private plans. That’s because most people who have long-term care insurance also have Medicare. And Medicare Part D is cheaper and more comprehensive than most private drug plans. Here’s the kicker: about 8.9% of long-stay Medicare residents in nursing homes have no drug coverage at all. They pay out of pocket-or rely on charity programs, family help, or temporary assistance. That’s nearly one in eleven people.

The Formulary Problem: Not All Generics Are Covered

Just because a drug is generic doesn’t mean it’s automatically covered. Every Part D plan has a formulary-a list of approved drugs. And not every generic is on every list. Some plans exclude certain generics because they’re not on the national preferred list, or because they’re newer and the plan hasn’t negotiated a price yet. Others might cover the brand-name version but not the generic, if the brand has a special rebate deal. That’s rare, but it happens. Nursing homes have to check each resident’s Part D plan before starting a new medication. They need to know:- Which plan the resident is enrolled in

- Whether their pharmacy works with that plan

- What drugs are on the formulary

- How to request an exception if the needed drug isn’t covered

What’s Changing? The $2,000 Cap and New Rules

Good news: starting in 2025, Medicare Part D beneficiaries won’t pay more than $2,000 out of pocket for drugs in a year. That’s thanks to the Inflation Reduction Act. For people on fixed incomes, this will be a huge relief. Also, as of 2021, CMS requires Part D plans to cover all drugs on the official Medicare Part D formulary for nursing home residents. And they must approve non-formulary drug requests within 72 hours for residents in long-term care. That’s faster than the old 14-day rule. Still, problems remain. Rural nursing homes often struggle to find pharmacies that contract with all major Part D plans. One in five rural facilities say they can’t get certain drugs quickly because their local pharmacy doesn’t work with their resident’s plan.What Should You Do?

If you or a loved one is moving into a nursing home:- Don’t assume long-term care insurance covers drugs. It doesn’t.

- Confirm enrollment in Medicare Part D. If they’re not enrolled, sign up immediately.

- Ask the facility which pharmacy they use and whether it works with the resident’s Part D plan.

- Get a copy of the drug formulary. Ask if the resident’s current medications are covered.

- If a needed drug isn’t covered, ask about the exception process. Don’t wait.

- Consider a Medicare Advantage plan with Part D included. Some offer better drug coverage than stand-alone Part D plans.

Why This Matters

Generic drugs make up 90% of prescriptions in nursing homes but only 25% of drug spending. That’s because they’re cheap. When a plan covers generics, residents get their meds on time and at low cost. When they don’t? People go without. They skip doses. They get sicker. They end up back in the hospital. The system isn’t perfect. But Medicare Part D has done more than any other program to ensure nursing home residents get the medications they need. The real issue isn’t whether long-term care insurance covers drugs-it’s whether we’re doing enough to make sure everyone has access to the right formulary, the right pharmacy, and the right support when they need it most.Does long-term care insurance cover generic drugs in nursing homes?

No, long-term care insurance does not cover any prescription drugs, including generics. It only pays for custodial care like help with bathing, dressing, and mobility. Drug costs are covered by Medicare Part D, Medicaid, or private health insurance.

Who pays for medications in a nursing home?

Medicare Part D covers about 82% of prescription drug costs for nursing home residents. Medicaid pays for residents who don’t qualify for Medicare. A small number pay out of pocket, and private insurance covers less than 9%. Most facilities bill Medicare Part D directly.

Are generic drugs always covered by Medicare Part D?

Most generics are covered, but not all. Each Part D plan has its own formulary, and some may exclude certain generics. Always check the formulary before moving into a nursing home. If a needed drug isn’t covered, you can request an exception.

What happens if a nursing home resident needs a drug not on the formulary?

The resident or their representative can request an exception from the Part D plan. As of 2021, plans must respond within 72 hours for nursing home residents. If denied, you can appeal. Delays can happen, so it’s best to confirm coverage before admission.

Will the $2,000 out-of-pocket cap in 2025 help nursing home residents?

Yes. Starting in 2025, Medicare Part D beneficiaries won’t pay more than $2,000 per year for drugs, no matter how many they take. This will protect residents from high costs, especially those on multiple medications for chronic conditions.

Can I use my long-term care insurance to pay for drugs if I run out of money?

No. Long-term care insurance policies are legally structured to exclude prescription drugs. Even if you’ve exhausted your funds, the policy won’t cover medication costs. You’ll need to rely on Medicare Part D, Medicaid, or financial assistance programs.

9 Comments

Lara TobinDecember 15, 2025 AT 15:23

Just had to move my mom into a nursing home last year, and this hit me right in the gut. We assumed LTC insurance covered meds until the pharmacy told us we owed $300 for her diabetes pills. I cried in the parking lot. 😔

Thank you for laying this out so clearly. I wish someone had told us this before we signed anything.

Keasha TrawickDecember 15, 2025 AT 20:51

Oh honey, this is the bureaucratic nightmare disguised as a safety net. 🎭

Imagine being a 78-year-old with five chronic conditions and your formulary changes mid-month because some insurance actuary decided generics from Manufacturer X are ‘non-preferred’-even though they’re chemically identical to the one you’ve been on for a decade. The nursing home staff are drowning in paperwork while you’re sitting there wondering why your blood pressure meds are suddenly ‘not covered.’

And don’t get me started on rural facilities where the only pharmacy that takes Part D is 40 miles away and closes at 4 p.m. on Tuesdays. We’re not fixing healthcare-we’re just moving the paperwork from one clipboard to another.

Alvin MontanezDecember 17, 2025 AT 08:31

Let me be perfectly clear: if you’re relying on long-term care insurance to cover pharmaceuticals, you’re not being prudent-you’re being dangerously naive. This isn’t some obscure fine print; it’s been the industry standard since the 1980s. The entire structure of LTC insurance is predicated on separating custodial care from medical care. That distinction exists for a reason: because medicine is expensive, and if you blur the lines, insurers go bankrupt.

Yet somehow, people still treat this like a gotcha. ‘Oh, they didn’t tell me!’ Well, you didn’t read the policy. You didn’t ask. You didn’t consult a financial planner. You assumed because you paid premiums, magic would happen. That’s not a flaw in the system-that’s a flaw in your expectations.

And before you say ‘but I’m elderly and overwhelmed!’-so is everyone else. The fact that you didn’t do your due diligence doesn’t make the system evil. It makes you irresponsible. Stop blaming insurers for your lack of planning.

Deborah AndrichDecember 19, 2025 AT 04:22

My aunt had to go without her Parkinson’s meds for 11 days because her Part D plan didn’t cover the generic and the exception request got stuck in limbo. She ended up in the ER. We had to beg the pharmacy to give her a week’s supply on charity.

It’s not about blame. It’s about broken systems. People aren’t lazy-they’re exhausted. We need to stop punishing the vulnerable for not being lawyers.

If a 75-year-old can’t navigate a formulary, the system failed-not them. Let’s fix the system. Not the people.

Scott ButlerDecember 20, 2025 AT 11:33

Of course Medicare covers it. That’s why we have Medicare. You people act like the government doesn’t pay for anything. You think this is some kind of conspiracy? It’s not. It’s called fiscal responsibility. If you want your pills covered, get on Medicare. If you didn’t, that’s your problem. Stop whining about private insurance not being a magic wand. We don’t need more bureaucracy-we need people to stop expecting free stuff.

And if you’re from another country and think this is bad? Try living in Canada. At least here, you get a shot at coverage. In some places, you get nothing. Be grateful.

Himmat SinghDecember 21, 2025 AT 08:22

It is imperative to underscore the fundamental distinction between custodial care and medical intervention. The contractual architecture of long-term care insurance is predicated upon the provision of assistance with activities of daily living, not pharmacological administration. To conflate the two is to misunderstand the actuarial basis of the product. The exclusion of pharmaceuticals is not an oversight; it is a deliberate, well-documented, and legally binding limitation. One must consult the policy document in its entirety, rather than rely on heuristic assumptions. The existence of Medicare Part D as a parallel mechanism renders this exclusion not only logical but necessary for system sustainability.

Bruno JanssenDecember 22, 2025 AT 15:30

I read this and just stared at the wall for 20 minutes.

I don’t know what to say. I just… I just keep thinking about my dad. He took seven pills a day. He never complained. He never asked for help. He just… swallowed them.

Now I’m wondering if he ever skipped one because he couldn’t afford it.

I don’t know how to fix this. I just… I just feel so hollow.

Emma SbargeDecember 24, 2025 AT 07:47

My sister works in a nursing home admin office. She says 3 out of 10 residents get denied a med at least once a month. Sometimes it’s because the pharmacy doesn’t take their plan. Sometimes it’s because the formulary changed without notice. Sometimes it’s because the resident’s family didn’t update the info after a Medicare switch.

It’s not a glitch. It’s the system.

And the staff? They’re the ones holding it together. They’re the ones calling pharmacies at 8 p.m. begging for a 3-day supply.

We treat these people like numbers. They’re not. They’re people. And they’re getting left behind.

Jamie ClarkDecember 25, 2025 AT 01:39

Let’s cut the fluff. This isn’t about insurance-it’s about who gets to live with dignity in America. We’ve turned healthcare into a game of financial Jenga, and the elderly are the bottom block. You think Medicare Part D is a solution? It’s a Band-Aid on a severed artery.

Generics are cheaper? Fine. But if your plan doesn’t cover the one your body actually tolerates, you’re forced to suffer, beg, or go without. That’s not policy. That’s cruelty disguised as economics.

And the $2,000 cap in 2025? Sweet. But what about the people who die before then? What about the ones who can’t wait for bureaucratic approval while their infection spreads? We don’t need more paperwork. We need moral courage.

This isn’t a policy problem. It’s a moral failure. And if you’re still defending the status quo, you’re part of the problem.